Budget 2026

Key Tax Changes for Business Owners and Investors

Here is a breakdown of the key tax announcements from Budget 2026 and what they mean for business owners and investors.

FBT on Vehicles

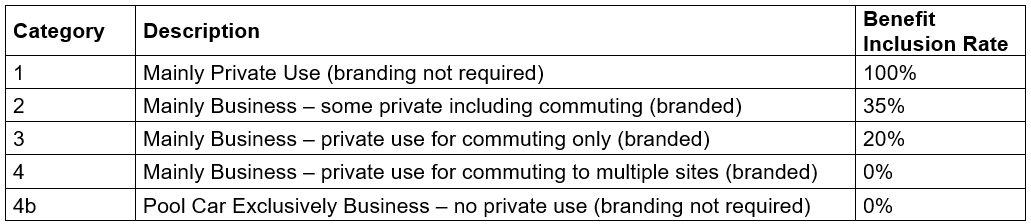

Effective from 1 April 2027, the Government is overhauling the Fringe Benefit Tax (FBT) rules for motor vehicles. The old system, where almost any private use of a work vehicle could trigger an FBT liability, is being replaced with a more practical, category-based approach.

This is a significant shift designed to reduce compliance costs and better reflect modern working arrangements.

Key Practical Changes for Your Business

No More Logbooks: The requirement to keep detailed logbooks to prove the split between business and private use will be removed, significantly cutting down on administration.

Branding is More Important: For vehicles to qualify for the lower FBT rates, they will likely still need to have the business’s name or logo permanently displayed. This helps demonstrate that the vehicle is a tool of the trade, not a private perk.

More Vehicles Can Qualify: A major change is that any type of vehicle can now potentially be treated as a work vehicle, not just traditional utes or vans. This means branded sedans or hatchbacks used for business could qualify for favourable treatment, which was difficult under the old rules.

New FBT Calculation Method: The way the value of the benefit is calculated will also change. A lower percentage will be applied to the value of hybrid and electric vehicles compared to petrol and diesel models, reflecting their lower running costs. This change aims to incentivise the uptake of greener vehicles.

For example, if your sales rep uses a sign-written sedan mostly for work but takes it home and uses it privately on weekends, you’ll likely only pay FBT on about 35% of the benefit instead of 100%. That’s a meaningful saving and much simpler to manage.

What this means: Less admin and more flexibility, but you must clearly define vehicle use policies.

Shareholder Loans

A new integrity measure is being introduced for companies removed from the Companies Register on or after 4 December 2025.

Under the new rule, any outstanding shareholder loan balance will become taxable income to the shareholder six months after the company is deregistered. This rule applies to loans made to shareholders, directors, and their close relatives. This is designed to prevent shareholder loans from being written off without tax consequences when a company is wound up.

Example: Sarah, the owner of Main Road Cafe Ltd, takes an $80,000 loan from her company.

Business slows, and Sarah has the company removed from the Companies Register on 1 February 2027. The $80,000 loan is still outstanding.

Under the new rule, the outstanding $80,000 loan balance is automatically treated as taxable income for Sarah six months after the date the company was removed from the register.

On 1 August 2027, Sarah is deemed to have derived $80,000 of income. She must include this amount in her personal income tax return for the 2027-28 tax year.

This ensures that the value Sarah received from the company is taxed in a timely manner, shortly after the company ceases to exist.

What should have been done instead:

1. Repay the loan; or

2. Declare a dividend (with imputation credits if available)

What this means: If you shut down a company and there’s still money owing to it by you or your family, Inland Revenue will treat that balance as taxable income six months later. You can’t just ‘walk away’ from shareholder loans.

Donation Tax Credits

The rules are changing for individuals who make significant charitable donations. A new cap will be introduced for donations made on or after 1 April 2027.

The eligible donation will be limited to the lower of:

1. $100,000; or

2. The person's total taxable income for the year.

For example, a person earning $500,000 who donates $500,000 to charity will have their rebate capped at $33,333 (33.33% of their $100,000 cap), not the $166,665 they might have expected previously.

What this means: Large donations will generate smaller tax refunds.

Not-for-Profit (NFP) Changes

Not-for-Profit organisations will see some benefits from the Budget.

Member Subscriptions Remain Non-Taxable: Following consultation, the Government has confirmed that member subscriptions and levies for mutual organisations will remain non-taxable.

Increased Automatic Deduction: From the 2027/28 income year, the automatic deduction available to NFPs increases from $1,000 to $10,000. This deduction is designed to cover minor amounts of taxable income (like bank interest) without creating a tax liability. This change, which has been requested for many years, will significantly reduce the tax and compliance burden for many small clubs and societies.

Simplified Filing: From the 2027/28 income year, if an NFP has no taxable income after applying the new $10,000 deduction, there will be no requirement to file an income tax return.

What this means: Many small clubs will no longer need to file tax returns.

Simplification of Foreign Investment Fund (FIF) Rules

For those with investments overseas, the budget introduces changes to simplify the FIF rules, effective from 1 April 2026.

Wider Access to a Simpler Method: The Revenue Account Method (RAM) will be expanded and made available to all New Zealand residents for their unlisted foreign shares. Under RAM, tax is only payable on realised gains (when you sell the shares) and dividends received. This moves away from the previous system which could tax unrealised "paper" gains, creating cash flow issues for investors.

Higher De Minimis Threshold: The threshold at which the FIF rules apply will be doubled from $50,000 to $100,000 (based on the original cost of the investments). This will remove many small investors from the complexity of the FIF regime entirely.

Example: In 2026, Alex invests in a portfolio of overseas shares. The total original cost, including brokerage fees, is $80,000. Alex’s $80,000 investment cost is below the new $100,000 threshold. He is now exempt from the FIF rules. This provides a significant compliance cost saving. Instead of performing complex FIF calculations, he will now only need to pay tax on any actual dividends he receives from his overseas shares.

What this means: Fewer investors affected and simpler compliance.

Foreign Currency Rules

To address complaints about being taxed on unrealised foreign exchange gains, the Government is introducing several changes to the financial arrangements rules from 1 April 2027.

These changes include:

Allowing some taxpayers to calculate their income in a foreign currency to reduce exposure to exchange rate fluctuations.

Removing common, low-risk foreign currency arrangements from the rules altogether, such as personal bank accounts, mortgages on private homes, and credit cards with foreign banks.

Special rules for those with Active Investor Plus visas

What this means: Less risk of paying tax without cash income.

Chester Grey comments:

For most taxpayers, this budget will not have a meaningful financial impact. The main takeaways are:

1. Reduced compliance (FBT, FIFs, Non-profit organisations)

2. Targeted tightening of integrity rules (shareholder loans, donation tax credits)

This Budget won’t change your tax bill dramatically tomorrow, but it will change how you need to manage certain areas going forward.

In particular:

Vehicle policies will matter more than logbooks

Shareholder current accounts cannot be ignored

Large donations require more planning

Offshore investments become easier but still need oversight

What should you do now?

1. Review vehicle usage (ahead of 2027)

Identify which vehicles are mainly business vs private

Consider whether Signwriting is appropriate

Consider whether EVs or hybrids make sense

Update internal policies for vehicle use

2. Check shareholder loan balances

Identify any overdrawn current accounts, especially in:

Dormant companies

Entities likely to be wound up

These must be cleared, repaid, or structured properly before deregistration.

3. Revisit donation strategies. High-income individuals making large donations should:

Reassess timing and structure

Consider spreading donations across years

While Inland Revenue has released fact sheets on these proposals, detailed information will not be available until the relevant legislative amendments are brought before Parliament.

If you have any queries in relation to the Budget proposals and their impact on you, please contact your Chester Grey advisor.